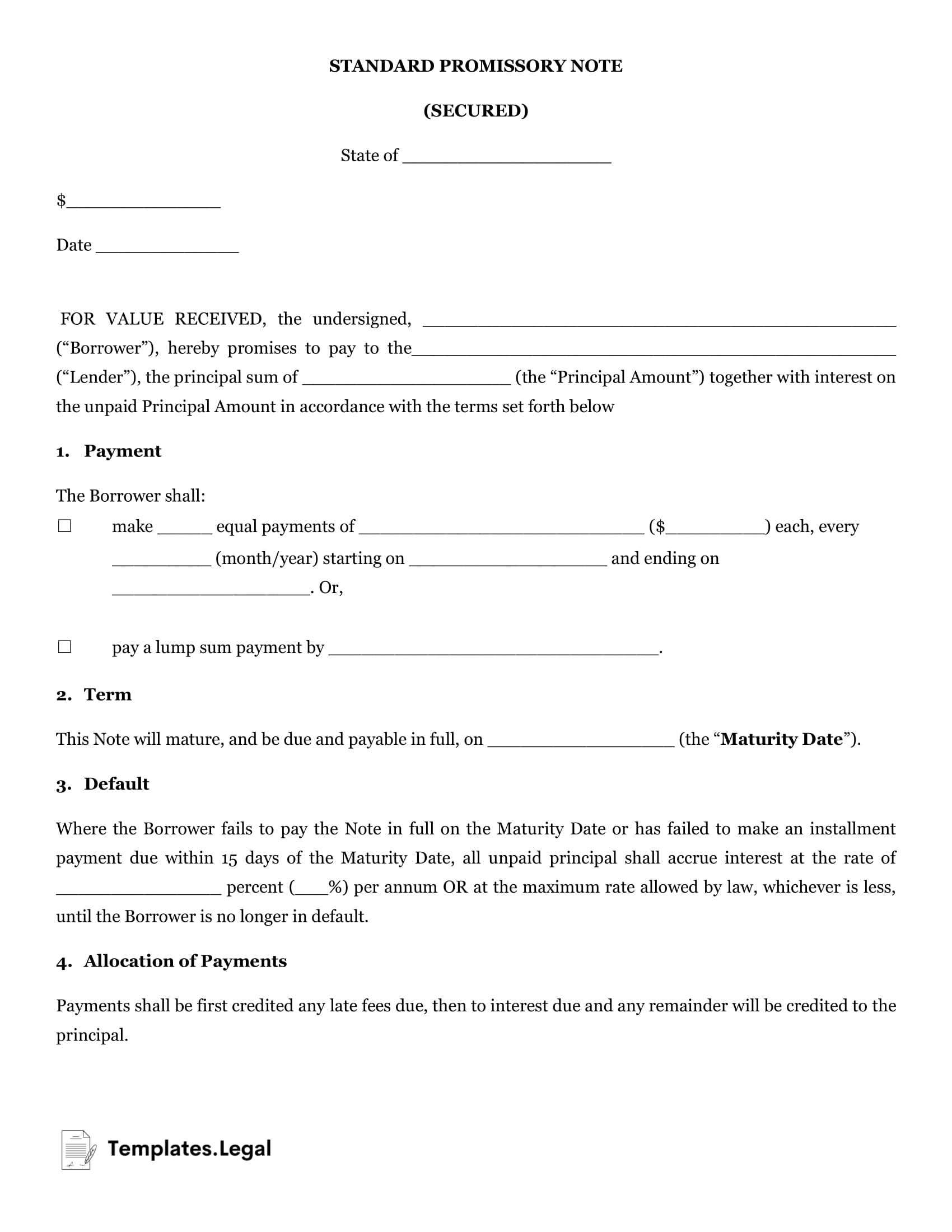

A promissory note can be an excellent way for both lenders and borrowers to benefit from a loan. A secured promissory note is a binding agreement between two parties, which guarantees repayment on an advance of funds. It is considered more potent than an IOU, but not always as strong as a formal loan agreement that you may get at a bank or another lending institution.

Promissory notes serve to mitigate the risk that the lender takes when they extend loan offers to borrowers in need. By having a binding document in hand, the lender has legal recourse to recoup any money lost due to nonpayment.

Contents hideAt a corporate level, loans secured by promissory notes can be a great investment opportunity for companies. However, those loans are typically substantial and are required to register with the SEC. You may also see promissory notes used during the closing stages of a house purchase when the borrower is seeking a mortgage.

There are two types of promissory notes – secured and unsecured. There are benefits to each, and you must decide which type of agreement works for your particular situation.

A secured note is also known as a promissory note with collateral. It is an agreement in which the borrower offers collateral, which can be claimed by the lender in the event of nonpayment. This collateral can take the form of a vehicle, real estate, or other valuable assets. The asset in question should always be equal to or greater than the value of the loan.

Any type of collateral does not guarantee unsecured promissory loans. Because those loans are typically riskier, they come with a higher interest rate to protect the lender. Typical unsecured loans that you may see are student loans and credit cards.

If you are considering lending a sum of money, it’s recommended to create a promissory note in the event of default. To do this, you can find a secured promissory note template which provides the details of the loan, and explicitly lists the asset being put up for collateral. If the borrower defaults, you have a legal document that entitles you to claim the borrower’s property as repayment.

Here are the steps for creating a reliable document which will protect you as a lender:

A promissory note on its own is not considered “secured” without a security agreement. If you opt for a secured promissory note over an unsecured note, you want to create a security agreement which makes reference to the loan and attach it to your document.

Be sure you provide as many details about the collateral as you can. For example, if a vehicle is being put up as security, including the make, model, color, and Vehicle Identification Number will guarantee that there is no mistake if you need to collect on a defaulted loan. As the lender, you will need to have your borrower sign a security agreement that contains this description and makes reference to the loan.

How Do I Secure a Promissory Note with Real Estate?A promissory note secured by real property can provide strong security for the lender, but it does come with a few additional steps. First, you must have the borrower sign the promissory note that you’ve already created, and make reference to the real estate being used as collateral.

Once the secured promissory note is signed, have the borrower sign a mortgage agreement that effectively puts a lien on the real estate, guaranteeing that it will be transferred to the lender in the event of default on the loan. Have this mortgage agreement signed, witnessed, and notarized to make it as enforceable as possible.

Lastly, you must file the promissory note and mortgage agreement with the appropriate office based on your state. Consult with an attorney to determine the proper filing method, whether that be with a town/county clerk or another local official.

What About Deeds of Trust?In some states, you must use a deed of trust in place of a mortgage agreement as security when financing a loan. A promissory note secured by a deed of trust functions in a very similar manner, except that a deed of trust is held by a third party government entity while a mortgage agreement is simply an agreement between the borrower and lender.

Check your state regulations about when to use a deed of trust when creating your secured promissory note.

How Can I Enforce a Breached Promissory Note?In the event that a borrower defaults on their loan agreement, the lender is entitled to collect the secured collateral that is guaranteed to them. They are free to repossess the secured asset through their own efforts, but it is often more effective to use professional agencies to accomplish this task.

If you choose to, you may file a petition with the courts. Assuming your promissory note and security agreements are in order, you should have no problem getting a judgment in your favor, which will strengthen your legal claim to the property.

As a final option, there are companies that specialize in purchasing defaulted promissory notes. The lender will receive a sum less than the value of the collateral, and the company will then attempt to collect on the debt through their own means.

Promissory notes do not need to be notarized for them to be legally enforceable, as long as both parties have provided their signature on the document.